Picture this: it is the first of the month, and instead of one manageable payment, you are staring down four or five credit card bills — each with a different due date, a different minimum, and an interest rate north of 20%. You pay the minimums, watch the balances barely move, and wonder if you will ever actually get ahead. If that scenario sounds painfully familiar, you are not alone. American households carried an average credit card balance of over $6,000 in 2026, according to recent Federal Reserve data.

The good news? There is a proven way out. Learning how to consolidate credit card debt can transform that pile of high-interest balances into a single, lower-rate payment — saving you hundreds or even thousands of dollars in interest and giving you a clear finish line for the first time in years.

In this guide — built on five decades of watching Americans dig their way out of debt — I will walk you through every consolidation method available in 2026, help you figure out which one fits your exact situation, and give you a step-by-step plan to get started today.

| Quick Answer: What Does It Mean to Consolidate Credit Card Debt? To consolidate credit card debt means combining multiple credit card balances into one single debt — ideally at a lower interest rate. This simplifies your payments and reduces the total interest you pay, helping you become debt-free faster. |

In This Guide: Balance transfers • Personal loans • Debt management plans • Home equity options • Step-by-step action plan • FAQ

Why Consolidating Credit Card Debt Is Worth Considering

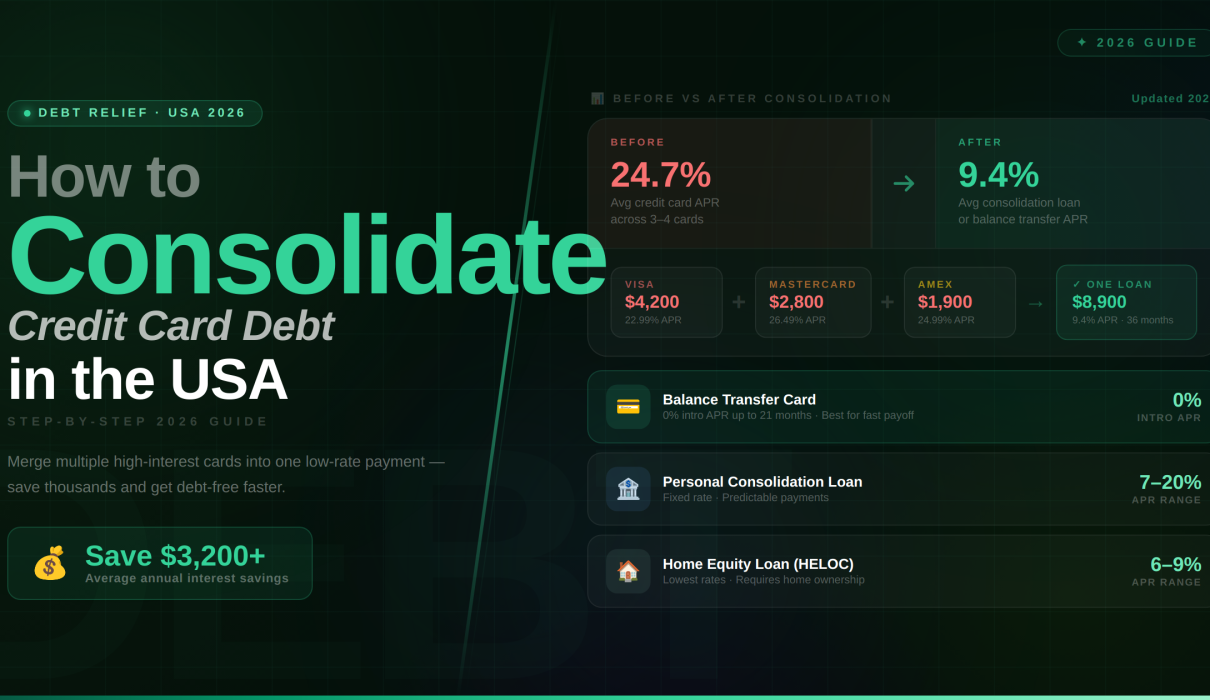

Before diving into the how, it helps to understand the why. The average credit card APR in the United States hovered around 21–24% in early 2026. That means for every $5,000 you carry, you are handing over roughly $1,000 to $1,200 per year — just in interest — while your balance barely budges.

Consolidation works because it attacks that interest rate directly. Instead of paying 22% across five cards, you might qualify for a personal loan at 10% or a 0% balance transfer card for 18 months. The math is not complicated — lower interest means more of every dollar you pay actually reduces your principal.

Beyond the financial math, there is a psychological dimension that gets overlooked. Managing one payment instead of five eliminates the cognitive load that leads to missed due dates, late fees, and credit score damage. Simplicity itself has real dollar value.

5 Ways to Consolidate Credit Card Debt in 2026

There is no single best method for everyone. Your credit score, total debt load, income stability, and timeline all factor into which approach makes the most sense. Here is an honest breakdown of every major option.

| Method | Best For | Credit Score Needed | Avg APR / Fee |

| Balance Transfer Card | Good credit, <$15K debt | 670+ | 0% intro (12–21 mo), 3–5% fee |

| Personal Loan | Large balances, stable income | 580+ | 8%–24% APR |

| Debt Management Plan (DMP) | High debt, fair credit | Any | 1–2% monthly fee |

| Home Equity Loan/HELOC | Homeowners, large debt | 620+ | 6%–9% APR |

| 401(k) Loan | Last resort only | N/A | Prime + 1%, penalties if default |

1. Balance Transfer Credit Card

A balance transfer card lets you move existing credit card debt onto a new card that offers a 0% introductory APR — typically for 12 to 21 months. During that promotional window, every dollar you pay goes directly toward your principal, not interest.

Best for: People with a credit score of 670 or higher who can realistically pay off the balance within the promotional period.

The catch: Most cards charge a balance transfer fee of 3–5% upfront. If your balance is $8,000 and the fee is 4%, you are paying $320 on day one. Still, that is usually far cheaper than 12–18 months of double-digit interest. Also, if you do not pay off the balance before the intro period ends, the remaining balance will typically be hit with the card’s standard APR — which can be just as high as what you left behind.

- Introductory APR: 0% for 12–21 months (varies by card)

- Balance transfer fee: typically 3–5% of the amount transferred

- Credit score needed: generally 670+

- Best when: you can pay off the balance before the promo period ends

If you are exploring this route, check our roundup of the best balance transfer credit cards for 2026 for current offers and terms.

2. Personal Loan for Debt Consolidation

A personal loan is a fixed-rate installment loan you use to pay off your credit cards in full, leaving you with one monthly payment at a set interest rate and a defined payoff date. Unlike a balance transfer card, there is no promotional window to race against — what you see is what you get for the life of the loan.

Best for: Borrowers with moderate to good credit (580+) who have a larger balance or prefer the predictability of a fixed payment schedule.

2026 rate landscape: Personal loan APRs ranged from roughly 8% to 28% in early 2026 depending on creditworthiness. Someone with excellent credit might lock in a rate around 9–11%, while a borrower with fair credit might see 18–24%. Even at the higher end, that often beats a 22% variable credit card rate.

- Fixed interest rate — no surprise increases

- Loan terms typically range from 24 to 84 months

- No collateral required in most cases

- Hard credit inquiry required when you apply

If your credit has taken a hit, do not assume you are disqualified. Our guide on personal loans for bad credit covers lenders who specialize in working with borrowers across the credit spectrum.

3. Debt Management Plan (DMP)

A Debt Management Plan is a structured repayment program offered through nonprofit credit counseling agencies. The agency negotiates directly with your creditors to lower your interest rates — sometimes dramatically — and consolidates your payments into one monthly amount you send to the agency, which distributes it to your creditors.

Best for: People carrying significant credit card debt who are struggling to qualify for a loan or balance transfer, or who want professional guidance through the process.

DMPs typically run three to five years. You will likely pay a small monthly fee (usually $25–$55) to the agency, but the reduced interest rates can make this option highly cost-effective. One important note: you will be required to close enrolled credit card accounts, which may temporarily affect your credit utilization and score.

If you are also weighing whether to attack multiple debts in a specific order, our comparison of the

debt snowball vs. debt avalanche methods can help you understand which payoff strategy fits your personality and math best.

4. Home Equity Loan or HELOC

Homeowners with meaningful equity have the option to borrow against their home through a home equity loan (a lump sum at a fixed rate) or a HELOC (a revolving credit line). Because the loan is secured by your home, interest rates are substantially lower than unsecured credit card debt — often in the 6–9% range in 2026.

The critical warning: This strategy converts unsecured consumer debt into debt secured by your house. If you run into financial trouble and cannot make payments, you risk foreclosure. This is not a method to take lightly. It makes sense only if you have strong financial discipline and a stable income.

- Significantly lower interest rates than credit cards

- Interest may be tax-deductible (consult a tax professional)

- Requires home equity and a credit score typically above 620

- Your home is at risk if you default

5. 401(k) Loan (Use With Extreme Caution)

Some retirement plans allow you to borrow against your 401(k) balance. Technically this can clear credit card debt quickly, and you pay interest back to yourself. It sounds appealing until you look at the fine print.

If you leave your job — voluntarily or otherwise — the outstanding loan balance typically becomes due in full within 60 days. If you cannot repay it, the IRS treats the outstanding amount as a distribution, which means ordinary income tax plus a 10% early withdrawal penalty if you are under 59½. You also lose years of compounding growth on the withdrawn funds. In my experience, this is a last resort, not a first move.

How to Consolidate Credit Card Debt: A Step-by-Step Plan

Knowing your options is the first step. Here is how to actually execute a consolidation strategy from start to finish.

- Get a complete picture of your debt. List every credit card balance, its current APR, and its minimum payment. Total it up. You cannot strategize around a number you have not faced.

- Check your credit score — for free. Your score will determine which options are available to you. Many banks and credit card issuers offer free credit score access. For a full report, you can check your credit score for free through AnnualCreditReport.com or your bank’s portal.

- Calculate how much you can realistically pay each month. A consolidation plan only works if you can make consistent payments. Be honest with your budget. Underestimating here is how people end up back where they started.

- Match your situation to the right method. High credit score + payable in under 18 months = balance transfer. Larger balance + fixed income = personal loan. Struggling with multiple creditors + need guidance = DMP. Use the comparison table above as your starting point.

- Apply and follow through. Once you consolidate, stop using the cards you paid off (or close them if you lack the discipline to keep them at zero). A consolidation loan used as a bridge to run up new balances is one of the most expensive financial mistakes you can make.

- Build a buffer. Even a small emergency fund of $1,000–$2,000 prevents the next unexpected expense from landing back on a credit card. If you need a framework, our guide on building an emergency fund from scratch walks you through it.

Will Consolidating Credit Card Debt Hurt Your Credit Score?

This is one of the most common questions I hear, and the honest answer is: it depends on the method, and any short-term impact is almost always outweighed by the long-term gain.

What may temporarily lower your score:

- Applying for a new balance transfer card or personal loan triggers a hard inquiry (typically -5 to -10 points, short-lived)

- Closing old credit card accounts reduces your available credit, which can increase your utilization ratio

- Enrolling in a DMP often requires account closures

What will improve your score over time:

- Lower credit utilization as balances decrease

- Consistent on-time payments building a stronger payment history

- Eliminating the risk of missed payments across multiple accounts

If your credit took a hit before you started this process, our guide on how to build your credit score fast covers actionable steps to accelerate recovery — including methods that work even if you are starting from scratch.

Common Mistakes to Avoid When Consolidating Debt

I have watched people follow every step correctly and still end up worse off two years later because of a handful of predictable errors. Here they are, so you can avoid them.

- Running up new balances on paid-off cards. This is the cardinal sin of debt consolidation. If you consolidate $12,000 of credit card debt and then charge $6,000 back up within a year, you have doubled your problem.

- Choosing a longer loan term just to lower the monthly payment. A 7-year personal loan at 15% will cost you far more in total interest than a 3-year loan at the same rate. Extend your term only if the lower payment is genuinely necessary to stay current.

- Ignoring balance transfer fees. A 5% fee on a $15,000 transfer is $750. Run the actual numbers before assuming a 0% card is your cheapest option.

- Not addressing the spending behavior that created the debt. Consolidation is a tool, not a cure. If the underlying habits do not change, the debt will return. A simple budgeting framework — like the 50/30/20 rule — can provide the structure you need.

- Working with a for-profit debt settlement company instead of a nonprofit credit counselor. Debt settlement is not the same as debt consolidation. Settlement companies often charge steep fees, can destroy your credit score, and sometimes leave you with significant tax liabilities on forgiven amounts.

What If You Have Bad Credit or No Credit History?

Not everyone entering this conversation has a pristine credit score, and that is completely normal. If your credit is damaged or thin, your options narrow — but they do not disappear.

A nonprofit DMP remains accessible regardless of credit score, since the agency negotiates on your behalf rather than extending new credit to you. Some lenders also specialize in debt consolidation loans for borrowers with fair credit, though the rates will be higher. And if you are working to rebuild your credit profile at the same time, a secured credit card can help you demonstrate responsible credit use while you work down your consolidated debt.

The key is not to let an imperfect credit score convince you that you have no good options. You may simply need a different starting point than someone with a 750 score.

Frequently Asked Questions

Is it a good idea to consolidate credit card debt?

For most people carrying high-interest balances across multiple cards, yes. Consolidation reduces your interest rate, simplifies repayment, and gives you a clear path to being debt-free. The key qualifier is that you must address the spending patterns that created the debt — otherwise consolidation becomes a temporary fix.

Does debt consolidation close your credit cards?

It depends on the method. A personal loan or balance transfer card does not require you to close existing accounts, though it is often wise to stop using them. A Debt Management Plan typically does require enrolled accounts to be closed as part of the agreement.

How long does it take to consolidate credit card debt?

The actual process of consolidating — applying for a loan, getting approved, and paying off your cards — can happen in as little as one to two weeks. The payoff timeline depends on your total balance and monthly payment. A focused borrower might clear $10,000 of consolidated debt in two to three years.

Will I save money by consolidating credit card debt?

In most cases, yes — often significantly. Moving a $10,000 balance from a 22% credit card to a 10% personal loan can save over $2,000 in interest over three years. The exact savings depend on your rate, balance, and how aggressively you make payments.

Can I consolidate credit card debt with bad credit?

Yes, though your options are more limited. A Debt Management Plan through a nonprofit credit counseling agency is available regardless of credit score. Some online lenders also offer personal loans to borrowers with scores in the 580–620 range, though at higher rates. If your credit needs rebuilding, starting with a secured credit card for no credit history can help you establish a positive payment track record while you work through your consolidation plan.

Bottom Line: How to Consolidate Credit Card Debt in 2026

After more than half a century of watching the financial decisions people make, I can tell you with confidence: consolidating credit card debt is one of the highest-return financial moves available to the average American. It cuts interest costs, creates clarity, and eliminates the psychological drain of juggling multiple creditors.

The best method for you depends on your credit score, your balance, and your timeline — but almost everyone carrying high-interest credit card debt has at least one viable path forward. The most important step is simply the first one: getting a clear picture of what you owe and making the decision to act.

If you are also trying to understand the broader strategy of getting out of credit card debt — including which accounts to tackle first — our detailed guide on how to get out of credit card debt walks through every approach in depth.

And if your credit score needs work before you qualify for the best rates, start with our guide on how to build your credit score fast — small actions there can unlock significantly better consolidation options within a few months.

| Ready to Take the First Step? Check your free credit score today, list your balances, and use the method comparison table above to identify your best path. Debt consolidation is not magic — but it is one of the most reliable tools available for reclaiming your financial life. |